Portuguese

Portuguese  Spanish

Spanish

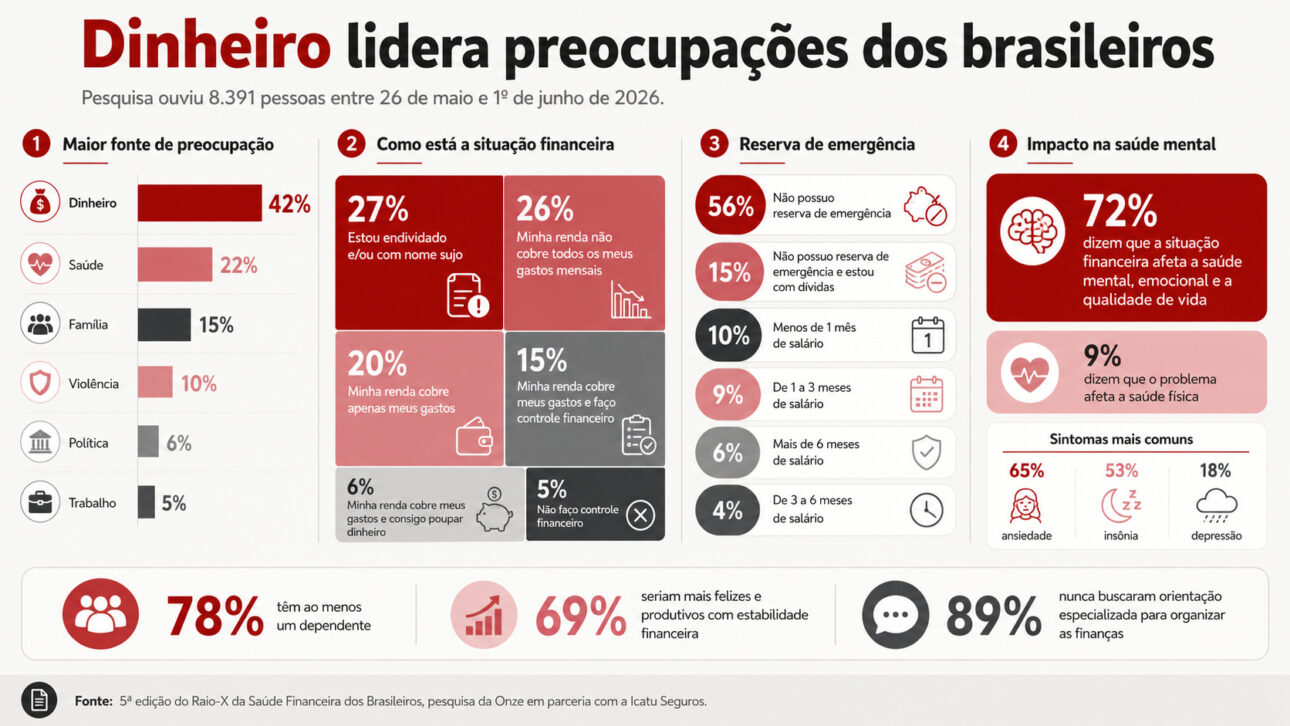

Survey shows that 42% of respondents point to money as the main concern, while 72% report impacts on mental and emotional health

Money has become the main source of concern for 42% of respondents in a survey on financial health.

The survey was conducted by the fintech Onze, in partnership with Icatu Seguros, between May 26 and June 1, 2026.

The survey interviewed 8,391 people, including employees with formal contracts, micro-entrepreneurs, unemployed individuals, business owners, retirees, and public servants.

-

Without Scalable Industrial Capacity, Brazil Risks Falling Behind, Warns Avibras Aeroco CEO as Company Resumes Missile and Drone Production and Prepares New Tactical Cruise Missile Launch

-

As 9,215 Brazilians Join Millionaire Ranks by 2025, 69% of Adults Still Have Less Than $10,000, Keeping Brazil Among World’s Most Unequal Nations

-

Entrepreneur Sells Car to Launch Healthy Meal Business, Now Runs Mr. Fit with 880 Stores in 3 Countries and $40 Million Annual Revenue

-

End of an Era: Renault Plans Major Overhaul, Cutting Jobs to Compete with Chinese Rivals and Transform Engineering by 2027

The results show that financial concern surpassed health, cited by 22%, family, with 15%, violence, with 10%, politics, with 6%, and work, with 5%.

Lack of savings increases insecurity and pressure on the budget

The absence of an emergency fund appears among the main problems identified by the survey.

About 56% of respondents stated they do not have money saved for unforeseen events.

Another 15% declared they have no savings and, at the same time, face debts.

Monthly income also represents a significant difficulty for a large part of the participants.

According to the survey, 53% stated that the money received does not cover all monthly expenses.

This group also includes people in debt or with a negative credit score.

Emergencies lead the biggest financial fears

The lack of resources to face unexpected situations worries 58% of respondents.

Health problems, accidents, and financial help to family or friends are among the main examples cited.

The difficulty in paying monthly bills comes right after, with 33% of the responses.

The assurance of a better future for their children worries 25% of the participants.

The settlement of debts or the removal of names from default registries was mentioned by 22%.

Credit card accounts for most of the debts

The credit card was pointed out by about 60% of indebted respondents.

The percentage considers installment purchases and bills that remain unpaid.

Personal loans appear in second place, with 30%.

Payroll loans, including Worker Credit, were mentioned by 26%.

The need to pay for food and basic bills explains the use of credit for 45% of respondents.

Unexpected emergencies, such as health issues or repairs, motivate 23% of loans.

Debt renegotiation or the attempt to clear one’s name appears as a reason for 13%.

Credit card can create a false sense of available income

Antonio Rocha, CEO and co-founder of Onze, states that the credit card can give the impression that there is more money available.

Spending beyond financial capacity makes it difficult to pay the full bill the following month.

The minimum payment, combined with interest, can turn the debt into a financial snowball.

Henrique Diniz, Product Director of Pensions at Icatu Seguros, also relates indebtedness to the constant stimulus of digital consumption.

Social networks and shopping platforms help maintain this incentive permanently.

Family responsibility increases the burden of bills

The survey revealed that 78% of respondents support at least one dependent, fully or partially.

Responsibility for other people increases the pressure on available income.

Dialogue about money at home is still infrequent.

More than half of the participants, about 53%, stated that they rarely talk about finances with family members.

The lack of financial protection also draws attention.

The survey shows that 63% do not have coverage for death or disability situations.

The search for specialized guidance is equally low.

About 89% have never sought professional help to organize their finances or get out of debt.

Financial stress affects mental health and productivity

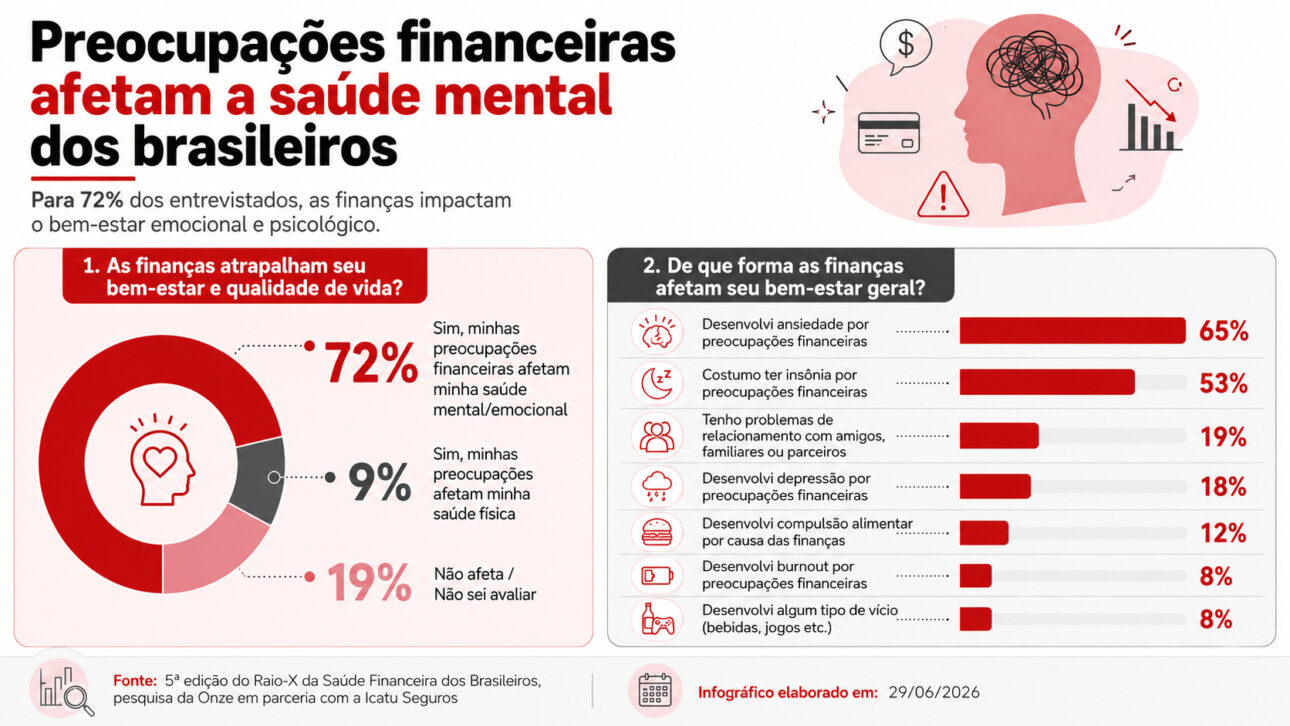

The financial situation harms the mental, emotional health, and quality of life of 72% of respondents.

Anxiety appears as the most common symptom, cited by 65%.

Insomnia was reported by 53%, while depression appeared in 18% of responses.

The effects also reach physical health in more severe situations.

About 9% reported feeling physical consequences caused by financial worries.

Antonio Rocha explains that anxiety and insomnia usually appear first.

Constant tension can also contribute to depression, physical problems, and eating disorders.

Financial stability can improve quality of life

The concern with bills, debts, and lack of savings keeps many people in a permanent state of tension.

The research shows that 69% believe they would be happier and more productive with greater financial stability.

Henrique Diniz states that financial stress also interferes with the work environment.

The fear of losing a job can further increase insecurity and reduce productivity.

The expert argues that companies and human resources sectors should discuss financial health with employees.

The provision of information, planning, and protection can help reduce worries inside and outside of work.

Nominal sources: fintech Onze, Icatu Seguros, Antonio Rocha, and Henrique Diniz.

In your opinion, what would help reduce financial stress the most: money education, card control, or income increase? Leave your comment.