Portuguese

Portuguese  Spanish

Spanish

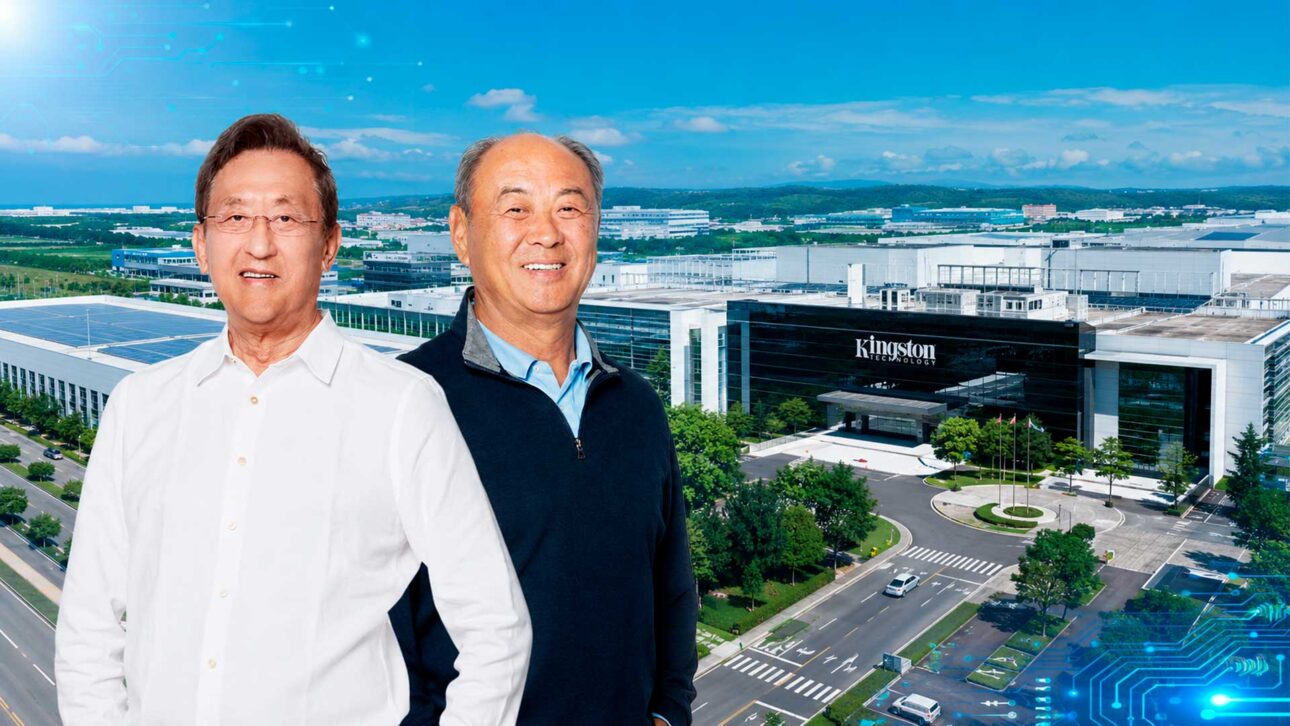

Kingston was born after an almost total loss on the stock market, passed through the hands of SoftBank, and returned to its founders for a fraction of the price

The story of Kingston Technology seems unlikely even by Silicon Valley standards. Two immigrant engineers, John Tu and David Sun, sold a majority stake in the company for $1.5 billion in 1996 and just three years later, bought back the same stake for $450 million.

Today, the company remains private, without the ups and downs of Wall Street, but holds a prominent position in the global market for memories, SSDs, cards, and storage solutions. In 2025, Kingston appeared on Forbes’ list of the largest private companies in the United States, with annual revenue of about $14.4 billion.

What makes this trajectory even rarer is that Tu and Sun not only regained control of the company. They did so in an extremely cyclical sector, where memory prices rise and fall according to demand for computers, servers, data centers, and more recently, artificial intelligence.

-

Government allows new ID to be requested via mobile phone for home delivery with CPF as a unique number: Rio has already issued 4.4 million IDs, the document is free, has a QR Code, biometrics, and replaces the old ID until 2032.

-

Panic in Times Square this Thursday: shots were heard in the heart of New York, the crowd ran in a desperate rush, and the police arrested the shooter with the weapon used.

-

Hidden 600 meters deep, giant concrete spheres can use ocean pressure to store clean energy and tackle the biggest bottleneck of solar and wind.

-

Pato Merlin becomes a phenomenon at the 2026 World Cup by wearing a Mexican jersey, garnering millions of views, and even challenging FIFA’s official mascots in popularity.

A friendship born on the basketball court paved the way for one of the most curious stories in technology

John Tu was born in China and David Sun was born in Taiwan. The two arrived in the United States in search of opportunities and ended up meeting in Los Angeles during basketball games before becoming partners in technology businesses.

Both studied electrical engineering and founded their first company, Camintonn, specializing in memory products. The business was sold in 1986 for about $6 million, an amount that seemed to guarantee a peaceful future.

But the tranquility was short-lived. After the stock market crash in 1987, known as Black Monday, the two lost a large part of the invested money. Instead of leaving the sector, they decided to start over.

It was in this context that Kingston Technology emerged, founded in 1987, in Orange County, California. According to Kingston itself, the company’s first product was a memory module developed for computers, at a time when PCs were beginning to spread through offices and homes.

The simple business that became a powerhouse without manufacturing its own chips

Kingston grew with a straightforward strategy. The company did not become a semiconductor manufacturer like Samsung, SK Hynix, or Micron. Its focus was on buying components, assembling memory modules, testing products, and delivering reliable solutions to consumers, businesses, computer manufacturers, and distributors.

This model may seem less glamorous than building billion-dollar chip factories, but it worked. In 1988, Kingston began offering a lifetime warranty on DRAM products, something uncommon at the time. In 1989, the company started individually testing its products, creating a strong reputation for quality.

According to Kingston’s official history, in 1995 the company surpassed $1.3 billion in sales. The following year, the company was already seen as one of the great success stories in technology in Southern California.

The logic was simple but difficult to execute: deliver reliable memory at scale, with technical support, good relationships with distributors, and attention to the corporate market. This combination placed Kingston in a privileged position just as personal computers, servers, and digital devices began to demand more and more memory.

SoftBank paid dearly at the peak and sold cheaply when the market changed

In August 1996, SoftBank, a Japanese group led by Masayoshi Son, bought 80% of Kingston for $1.5 billion. Tu and Sun continued to lead the management and retained a 20% stake in the company.

The deal attracted attention not only for the value. The founders decided to distribute $100 million in bonuses to employees, a gesture that became a symbol of Kingston’s internal culture and reinforced the image of a company growing without breaking away from its roots.

But the memory market changed rapidly. The sector is known for cycles of scarcity and oversupply. When there is a shortage of components, prices rise and margins increase. When supply grows too much, prices fall sharply.

It was this environment that opened the way for an unusual turnaround. In July 1999, Tu and Sun would buy back the same 80% of Kingston for $450 million, a third of the sale value three years earlier. At that time, SoftBank wanted to concentrate capital in internet companies, while Kingston was still facing the effects of falling memory prices.

The buyback returned control to the founders of a company that continued to grow

The buyback of Kingston became a rare case of “selling high and buying low” in the technology world. Tu and Sun received a fortune from the sale, maintained influence in the operation, and then regained control for a much lower value.

The difference is that Kingston did not disappear after the transaction. On the contrary. The company expanded its operations in memory cards, pen drives, SSDs, DRAM modules, products for gamers, encrypted solutions, and corporate storage.

According to Kingston, the company entered the flash card market in 1999, launched its first USB drives in 2001, and created the Kingston Digital division in 2003. These decisions helped the company keep up with the market shift from traditional desktop computers to digital cameras, notebooks, cell phones, servers, data centers, and connected devices.

This point explains why Kingston’s story is not just a financial curiosity. The company has gone through various phases of technology while maintaining a private structure and control in the hands of the founders.

Artificial intelligence has placed memory and storage at the center of the new technological race

The recent growth of artificial intelligence has once again placed memory and storage at the center of the industry. AI models, data centers, and cloud services require enormous volumes of DRAM, NAND, SSDs, and high-speed solutions.

In a report cited by Kingston in October 2025, Kingston maintained global leadership among third-party DRAM module suppliers in 2024, with 66% estimated revenue share. The same survey indicated that the DRAM module market grew by 7% in 2024, after a decline the previous year.

The industry’s own dynamics help explain the company’s new strategic value. When manufacturers prioritize high-bandwidth memories and DDR5 for servers, other types of memory may become tighter, driving up prices and increasing the importance of companies capable of distributing products at scale.

In 2026, Tu and Sun saw their fortunes grow with the wave of demand for AI-related memory. The publication pointed out that the two remain equal owners of Kingston, a rare detail in an industry marked by IPOs, funds, mergers, and acquisitions.

Kingston shows how a discreet company became a giant without going public

Kingston does not have the same visibility as giants like Nvidia, Microsoft, or Apple, but its products are present in computers, notebooks, servers, cameras, cell phones, IoT devices, and corporate systems. It is the type of company that works behind the scenes of technology but supports an essential part of the digital infrastructure.

In January 2026, Kingston announced that it rose to the 28th position on the Forbes list of largest private companies in the United States in 2025. The company also stated that it remains the leading company in the hardware and technology equipment category within the ranking.

The case draws attention because Tu and Sun followed a different path from the traditional Silicon Valley script. They did not go public, did not hand over control to external investors, and did not turn the company into a noisy acquisition machine.

Kingston grew more quietly, based on product, distribution, quality, and customer relationships. And precisely because of this, it became an example of how a company can become a giant without being in the headlines every day.

An almost total loss became the beginning of an even greater fortune

The journey of John Tu and David Sun combines crisis, timing, discipline, and a rare dose of business patience. They lost money in the 1987 crash, founded a company in the same year, sold most of it in 1996, and bought back control in 1999 for a much lower value.

More than three decades later, Kingston remains relevant because it operates in one of the most sensitive points of the digital economy: memory and storage. Without these components, computers, cell phones, servers, cloud, and artificial intelligence simply do not function at the scale required by the current market.

The story also shows that not every tech giant is born from apps, social networks, or electric cars. Sometimes, the empire lies in small parts, almost invisible to the average consumer, but indispensable to keep the digital world running.

Do you think Kingston’s buyback was genius, luck, or a mix of both? Leave your opinion in the comments and tell us if you already knew the story of John Tu, David Sun, and the company behind so many memories and SSDs used worldwide.

Be the first to react!