Portuguese

Portuguese  Spanish

Spanish

Account Blocks for “Security” Without Court Order Increase With Financial Digitization and Clash Compliance Duties and Customer Rights; Central Bank Decisions and Standards Detail When the Measure Requires Indemnification.

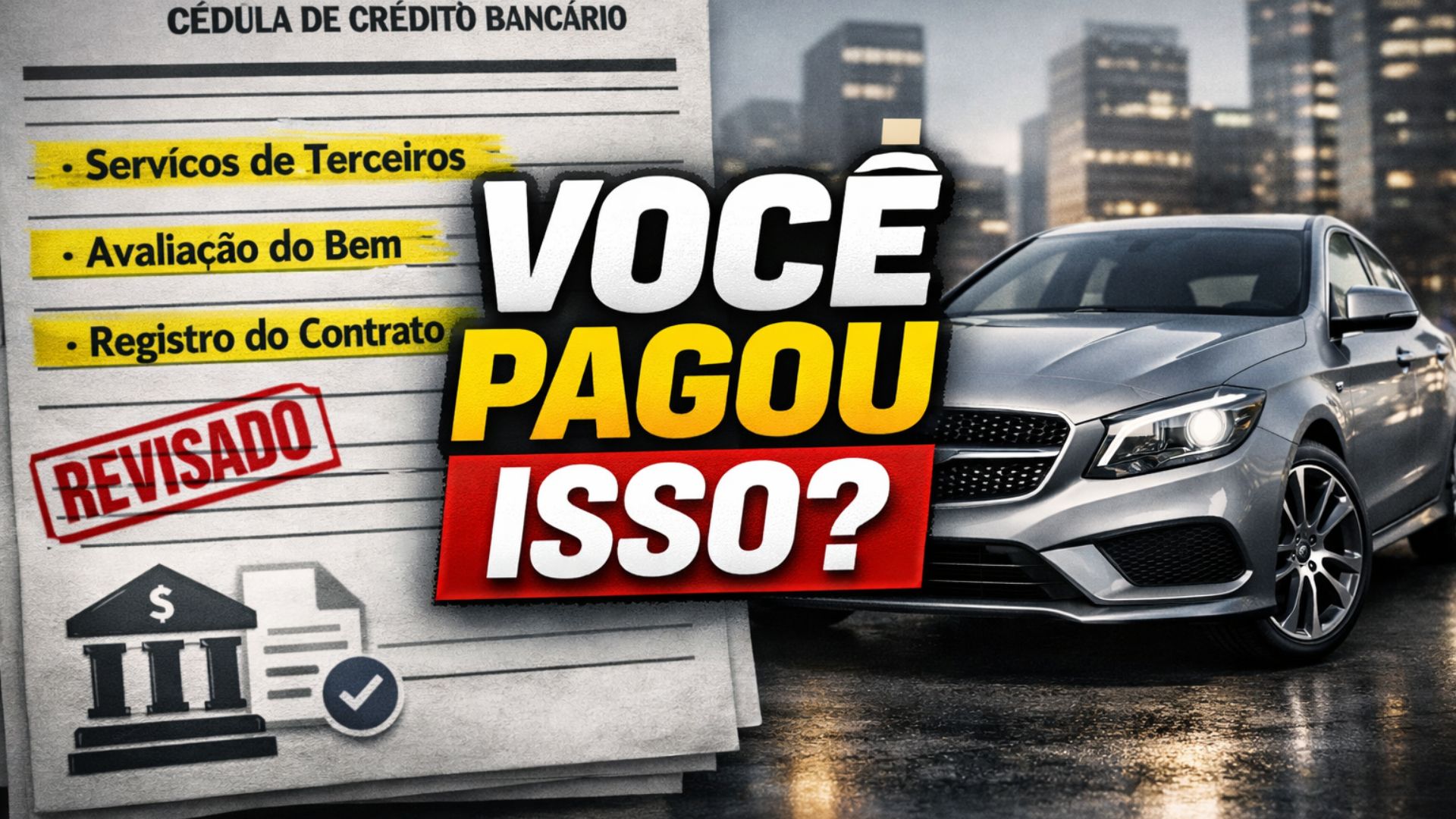

Understanding of the STJ About Fees in Vehicle Financing

The Superior Court of Justice established theses under the repetitive appeals process that guide, throughout the country, when fees charged in vehicle financing should be maintained or refunded.

The judgment, known as Theme 958, settled three central points: generic charging for “third-party services” is abusive if there is no specification and proof of what was effectively provided; the commission for the banking correspondent is prohibited in contracts signed from February 25, 2011, the date of validity of Resolution CMN 3.954; and the property evaluation fee and contract registration expenses are valid as long as the service has been performed and there is no excessive burden.

State courts have been applying these guidelines, determining the restitution of amounts when the institution does not prove the provision of the service or describes the charge vaguely.

-

Brazilian City Makes Remarkable Leap, Becomes 4th Wealthiest in the Country with GDP of R$ 134.1 Billion

-

Controversial 6-day Workweek Elimination in Brazil Faces Economic Criticism Over Productivity Claims

-

Itaú to Refund Customers After 14 Years of Unauthorized Credit Card Charges; Agreement Includes No Interest or Adjustments, Deadline by 2028, with Potential Impact of Up to $6.5 Billion

-

Brazilian Company Grows from Bartering Soap for Food to Producing 30 Million Units Monthly, Challenges Global Giants with $100 Million Revenue and Expands into Premium Cosmetics

Repetitive Appeals and Standardization of Decisions

In practice, the understanding of the STJ has started to guide contract reviews because the decision in repetitive binds identical cases in lower courts, reducing divergent decisions.

The thesis does not prohibit, by itself, the charging of all analyzed fees but imposes an objective filter: each item needs to have documentary support, a clear description in the contract, and correspondence with a real service performed for the consumer.

Without these elements, the charge tends to be considered undue, which opens space for simple or double restitution, depending on the evidentiary discussion regarding bad faith, in addition to any monetary correction according to criteria defined in the processes.

“Third-Party Services” and Banking Correspondent

The most sensitive point is the item “third-party services”.

The broad label is not sufficient, by itself, to transfer costs to the consumer.

When the institution uses this expression generically, without detailing the type of activity performed, the provider, the contractual link, and the benefit to the contractor, the charge is deemed abusive.

The guidance also distinguishes “third parties” from “banking correspondents”: from February 25, 2011, the commission for the correspondent became subject to specific regulatory restrictions, preventing its pass-through to the consumer during this period.

In contracts prior to that date, validity depends on a specific examination of burden, maintaining the need to demonstrate the service.

Property Evaluation Fee and Contract Registration

The property evaluation fee and the contract registration expenses have been recognized as, in principle, admissible.

The evaluation of the property refers to the technical verification of the vehicle given as collateral, a procedure that may involve inspection, documentation verification, and pricing for risk assessment.

The contract registration refers to the annotation of the encumbrance with the competent agency, making the bond public and protecting the fiduciary guarantee.

In both cases, the STJ established that the charge only stands if there is proof that the services were effectively executed, with a compatible price and without excessive burden.

In the absence of proof, the charge can be dismissed and reimbursed.

Where to Find Charges in the CCB

The contract that materializes these charges is generally the bank credit note (CCB) issued at the time of financing.

It is in this document, accompanied by the summary table and the financial statement, that the lines related to “third-party services,” “property evaluation,” “contract registration,” “electronic lien,” and “notary expenses” appear.

In digital contracts, the same fields are usually included in PDFs attached to the contracting file.

The absence of clear identification of the nature of the service, the provider, and the itemized value hinders verifying legitimacy and, in light of the repetitive theses, weighs against maintaining the charge.

When there is an indication of an agent or specific company responsible for registration, for example, the institution must present work orders, invoices, or proof of payment to support the fee.

How the Courts Have Applied the Theses

State courts have been aligning decisions to this standard.

In recent rulings, courts confirmed that “third-party services” described generically constitute undue charges, while they upheld the property evaluation fee and registration expenses when the institution presented documents from the technical report and the payment of fees to the registration agency.

Conversely, when the bank did not demonstrate the performance of the evaluation or did not prove the registration, the courts determined the restitution of the amounts.

Although the amounts vary according to the contract and the location, the decision-making logic has remained: without proven provision, there is no basis to maintain the charge.

Contractual Transparency and Duty of Information

The standardization promoted by the STJ also aligns with norms of the National Financial System that address transparency and information in banking services.

Regulations from the Central Bank and the Monetary Council require contracts to clearly indicate prices and the nature of the charged services, which helps mitigate conflicts.

In the consumer sphere, the duty of information and the prohibition of abusive clauses support the analysis of the validity of the fees.

The principle that emerges from this intersection is objective: the cost can only be passed on to the consumer if it corresponds to an essential service to the operation, performed and proven, without transferring inherent risks or expenses of the supplier’s activity to the contractor.

How the Consumer Can Identify Undue Charges

For the consumer, identifying possible undue charges begins with examining the bank credit note and the summary table, paying attention to items that do not clearly describe the service.

In financings signed after February 25, 2011, the presence of a banking correspondent’s commission passed on to the contractor contradicts the established understanding.

In cases where the institution indicates evaluation and registration, the compatibility of the value with market practices and the existence of supporting documents are relevant criteria.

When the charge cannot be sustained, judicial decisions have determined restitution and, in some cases, a review of the contract’s calculations.

Necessary Distinctions and Limits of the Theses

The repercussions of Theme 958 do not alter charges that have their own regime, such as the registration fee, whose validity follows a specific understanding defined by the STJ in another repetitive and by regulations of the Monetary Council.

This distinction is relevant to avoid confusion between charges of different nature and grounds.

There is also no authorization in the theses for the use of abstract “excess” parameters without support in objective elements.

The control of excessive burden requires comparison with practiced values and the actual need for the service, always in light of the evidence in the process.