Portuguese

Portuguese  Spanish

Spanish

BR Petrobras Loses Leadership in Brand Strength; Ipiranga and Shell Lead Convenience Stores; Vibra Faces Immediate Rebranding Challenge.

BR Petrobras loses its leadership in Brand Strength, with Vibra facing the imminent challenge of rebranding. Ipiranga and Shell are now leading in the convenience store and gas station market, taking the lead of the strongest brand in this dynamic sector.

The fierce competition between Ipiranga, Shell, and BR Petrobras is redefining the branding landscape in Brazil, with each company seeking to strengthen its logo and brand identity. Vibra needs to undertake significant rebranding efforts to maintain its relevance in this competitive environment.

Dominant Presence of Brands in the Fuel Market

In Brazil, three major brands account for approximately 82% of the main consumers in the fuel market. They are BR Petrobras, operated by the Vibra Energia group, with a 30.6% share, Ipiranga, from the Ultra group, with 29.5%, and Shell, owned by the Raízen group, which holds 22.3%. Other smaller networks, such as ALE, Total Energies, Carrefour, Atacadão, Assaí, among others, share the remainder of this competitive market.

-

The Chamber releases R$ 10 billion to hold the price of diesel until December and proves that Brazilian fuel remains tied to Congress.

-

It’s official: Petrobras takes 75% of block 3 in São Tomé and Príncipe and debuts as an offshore operator outside South America.

-

With a record production of nearly 3 million barrels per day, Petrobras resumes importing diesel in July, highlighting the bottleneck in Brazilian refining.

-

Qantas and Airbus Invest in Company Aiming to Convert Unsorted Household Trash into Jet Fuel

Brazil currently has over 40 thousand fuel stations, according to ANP, and about 8 thousand convenience stores that offer a variety of products and services, including fuels, lubricants, automotive services, food, beverages, and tobacco, among others.

Decisive Factors in Choosing Gas Stations

Location, competitive prices, good brand reputation, presence of convenience stores, short lines, fuel quality, well-maintained facilities, helpful attendants, and effective loyalty programs are attributes that significantly influence consumers’ choices of their preferred establishment.

The three leading brands stand out due to their larger number of stations, long market presence, and continuous investments in communication, convenience stores, and loyalty programs. CVA Solutions, a division of the American CVM Inc., which has operated for 23 years in Brazil and 28 in the United States, recently completed a detailed analysis of this segment.

Market Study and Main Business Axes

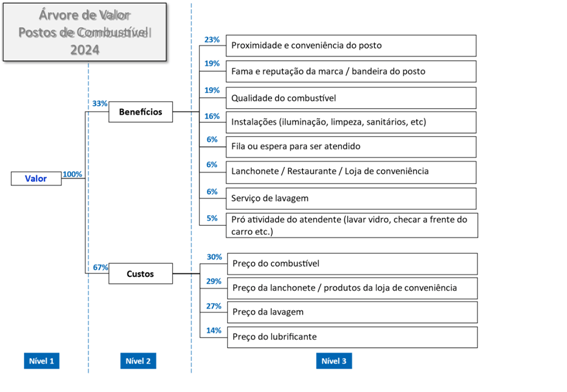

Through a comprehensive online survey, the consultancy examined the main business axes, marketing, and services based on the opinions of 4,266 people across the country, covering all income levels and ages in all Brazilian states. The survey addressed Perceived Value, NPS (Net Promoter Score), and Brand Strength, providing insights into the customer journey at the gas station.

The Perceived Value considers the cost-benefit assessed by customers. Among the respondents, benefits accounted for 33% of the perceived value, with highlights on location (23%), brand reputation (19%), fuel quality (19%), physical facilities (16%), lines (6%), convenience store (6%), car wash service (6%), and attendants (5%). Costs weighed 67%, highlighting fuel prices (30%), snack bar prices (29%), car wash prices (27%), and lubricant prices (14%).

The Impacts of the Customer Journey and Rebranding

Customers tend to pay a little more for fuel if they avoid long lines, receive good service, and find a good convenience store, according to Sandro Cimatti, CEO of CVA Solutions. Perceived Value along with NPS allows measuring the customer journey. Satisfied consumers tend to recommend the brand, expanding its presence.

In terms of perceived value, Ipiranga leads, followed by Shell, BR Petrobras, Assaí, ALE, Total Energies, Atacadão, and Carrefour. In NPS, Ipiranga also leads with 64.5%, followed by Shell, BR Petrobras, Carrefour, Total Energies, ALE, Atacadão, and Assaí. Brand Strength, which reflects the degree of recognition and attraction of customers, ranks Ipiranga in the first position, followed by BR Petrobras, Shell, Atacadão, Assaí, Carrefour, Total Energies, and ALE.

Challenges and Strategies of Vibra Energia

BR Distribuidora, with a network of over 8,300 stations, was acquired by Vibra Energia in 2021. In January 2024, Petrobras communicated to Vibra that it does not intend to renew the brand license after the contract ends in June 2029. CVA’s research identifies that the Vibra brand is not well known, with recognition of only 19.1% among general consumers and specific BR Petrobras consumers. When prompted, the association of the Vibra brand with the BR Petrobras network increases.

BR Petrobras has lost its leadership in brand strength and has less communication recall than Ipiranga and Shell among its consumers. ‘This is a crucial moment for Vibra Energia. It doesn’t make sense to invest in communication for the BR Petrobras brand with the possibility of not being able to use it in the future; however, failing to invest in it could weaken the brand,’ explains Sandro Cimatti. The ideal solution seems to be an immediate rebranding, migrating the BR Petrobras brand to Vibra Energia, with a five-year transition plan.

Profitability and Loyalty Through Services

The CVA study reveals that convenience stores and automotive services are essential for increasing profitability and loyalty of gas stations. About 40.8% of fuel station customers visit convenience stores, and these consumers utilize more lubricant changes and car washes compared to those who do not frequent such stores. Ipiranga leads in these services, followed by Shell and BR Petrobras.

Lubrax (BR Petrobras) leads in lubricant sales, followed by Mobil, Castrol, Ipiranga, and Shell. In loyalty programs, Ipiranga leads, followed by Shell and BR Petrobras. ‘The fuel retail market is less digitalized and loyal compared to that of pharmaceuticals and food, so convenience stores and loyalty programs are effective strategies to bring consumers closer to the brand,’ concludes Cimatti.

Source: © paula@difattocom.com.br

Cessão de marca lesiva à Petrobrás. A Vibra, quando tem vazamento e acidentes, não se apresenta, preferindo queimar a marca Petrobras. Fica parecendo que o acidente aconteceu em instalações da Petrobrás, vide o caminhão que explodiu em pleno bairro densamente povoado no Rio de Janeiro.

Valor da cessão também foi irrisório, e mais: contraditório na essência, pois nem a gasolina da Vibra é da Petrobras.

Já passou da hora da vibra parar de queimar o nome Petrobras e seguir com as próprias pernas.

Mas graças aquela tranqueira do Bolsonaro e Paulo Guedes e CIA, que cederam a marca BR Petrobras,Lubrax, br conveniência, por 8 anos.

Caso não saibam, a vibra é a Br Petrobrás, nunca existiu Vibra antes. A Br Petrobrás que mudou para Vibra, pois foi a holding mãe, que passou a utilizar a marca Br por ela ter ficado tão forte por causa da distribuidora que após ter suas ações vendidas passou a se chamar Vibra energia.

A holding vendeu o ativo e não a marca.

Atualmente nem o combustível é Petrobras mais… é quase um posto sem bandeira kkkk

Bruno Morais tem razão com as “tranqueiras”…

Está desinformado. A marca não foi cedida, existe contrato de uso de marca e a Petrobrás recebe por isso. Ninguém cede nada em negócios.

A reportagem vem com dados inexatos. A Vibra é a BR Distribuidora que mudou de nome.

Exatamente isso, meu camarada.