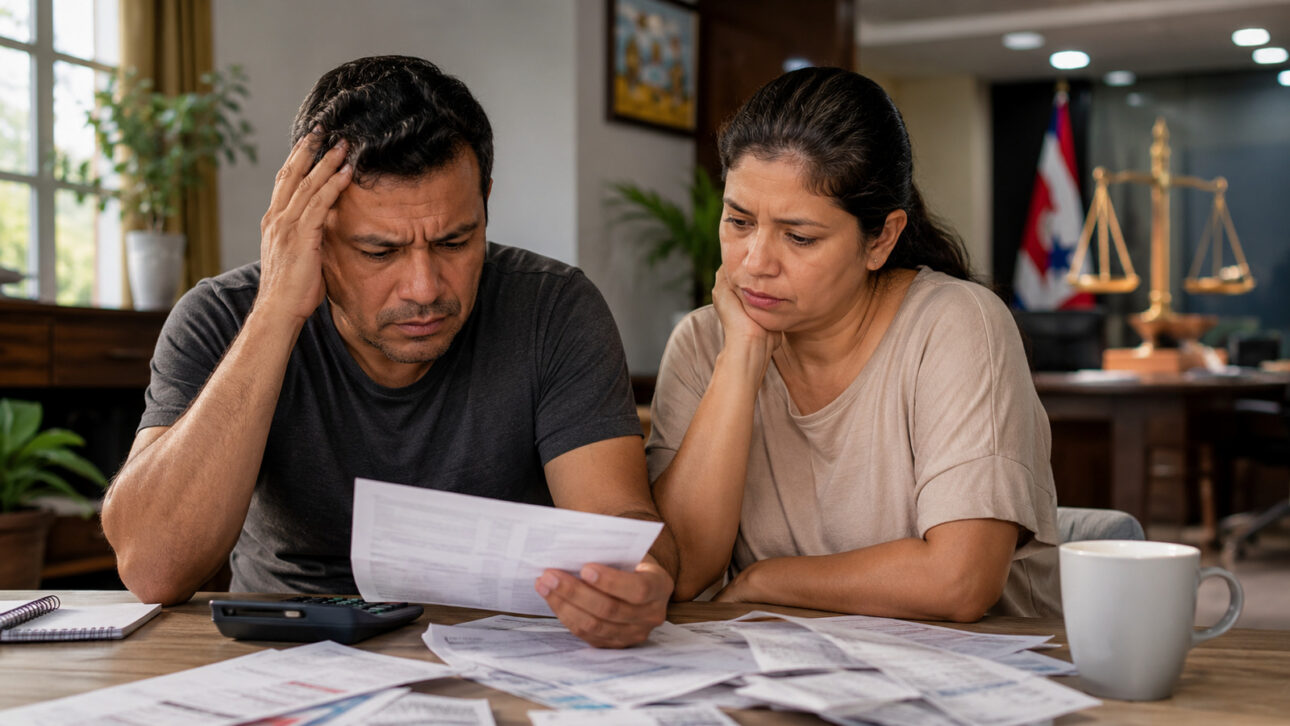

New state law aims to prevent and address over-indebtedness in Pará with educational campaigns, debt renegotiation, Procon support, and financial guidance for consumers who have lost control over their own income

The Over-Indebtedness Combat Law in the State of Pará, Law No. 11,530, is already in effect after being signed by Governor Hana Ghassan, according to O Liberou published yesterday (15). The new public policy provides for educational actions, monitoring of abusive practices, and encouragement of debt renegotiation at a time when 80.9% of Brazilian families declared having some type of debt.

Over-Indebtedness Combat Law provides for prevention and treatment of debts

The new state law creates a public policy aimed at preventing and treating the over-indebtedness of consumers in Pará.

The goal is to tackle situations where a person cannot pay their debts regularly and predictably due to their financial condition.

-

Itaú holds an auction of 200 properties in June with prices starting at R$ 43,000 and discounts of up to 63%.

-

Brazil refuses to support the G7 text on critical minerals and rare earths, enters the heavy game of strategic inputs, and tries to escape the old trap of exporting raw wealth while rich countries keep the most profitable part.

-

São Paulo accelerates basic sanitation with R$ 70 billion until 2029, expands treated water, sewage, and promises to advance universalization four years ahead of the national deadline.

-

A Russian franchise group chose Brazil to expand its capybara-themed autonomous coffee shop because Brazilians drink four times more coffee than Russians, and the company aims to reach 600 units by December 2026, although it currently operates only 15 locations.

Among the measures provided are educational campaigns on financial education, responsible use of credit, and personal finance organization. The law also addresses consumer guidance on the risks of excessive indebtedness.

The text also provides for the regulation of practices such as tied selling and the monitoring of abusive supplier conduct.

Another point is the encouragement of debt negotiation and renegotiation, with the possibility of loan contract review.

Procon and financial counseling services should be strengthened

To implement the public policy, Law No. 11,530 provides for the strengthening of state consumer protection agencies, such as Procon. The measure also encourages the creation of specialized financial counseling services.

These actions are aimed at consumers who have already lost the ability to organize debt payments within their available income. The proposal includes guidance, renegotiation, and prevention to prevent the problem from advancing.

According to the consulted material, the Pará law follows a national agenda linked to the growth of family indebtedness.

In April 2026, the Consumer Debt and Default Survey by CNC indicated that 80.9% of Brazilian families had some type of debt.

When debt becomes over-indebtedness

According to Law No. 11,530, over-indebtedness is the situation where the consumer is unable to pay their debts regularly and predictably due to their financial situation.

The professor and economist from Pará, André Cutrim Carvalho, explains that the problem goes beyond a late bill. According to him, it occurs when the set of debts consumes income to the point of compromising basic expenses.

“It’s not just about owing or having a late bill, but a situation where the set of debts consumes income to such an extent that the person can no longer maintain basic expenses, such as food, housing, energy, transportation, health, and education,” he stated.

Among these expenses are food, housing, energy, transportation, health, and education. The economist states that the situation arises when a person loses control over their own income and starts incurring new debts to pay off old commitments.

He also mentions the frequent use of credit cards, overdrafts, and loans to cover daily expenses. In many cases, the income is already compromised even before receiving the salary.

“In practice, this problem starts to appear when a person loses maneuverability over their own income, starts making new debts to pay off old commitments, frequently resorts to credit cards, overdrafts, or loans to cover daily expenses, and ultimately, loses clarity about the total amount owed and, in many cases, starts living with a significant portion of their income already committed before even receiving the salary,” he concluded.

Loss of income, interest rates, and online betting exacerbate the problem

André Cutrim Carvalho states that over-indebtedness should be seen as an economic and social problem.

According to him, it does not result solely from a lack of financial planning, but also from loss of income, unemployment, health problems, high interest rates, and excessive credit offers.

The economist also points to the rise of online betting, known as bets, as a recent aggravating factor.

According to him, families resort to these platforms trying to supplement their income or get money to pay off debts, which can worsen the financial situation.

The financial analyst in consultancy Ana Paula Matos Leal recommends that over-indebted individuals acknowledge the situation and reorganize their financial life. She advises listing sources of income, essential expenses, and all existing debts.

“For people who are already over-indebted, the first step is to recognize the situation and seek to reorganize their financial life. It is advisable to list all sources of income, identify essential expenses, and map all existing debts, establishing priorities for paying the most urgent commitments. It is also crucial to avoid taking out new loans to pay off old debts, a practice that tends to worsen the problem and prolong the cycle of indebtedness. In this context, seeking negotiation channels and financial guidance services becomes an important measure for building sustainable solutions,” points out the analyst.

Ana Paula also recommends establishing priorities to pay urgent commitments and avoiding new loans to pay off old debts.

For her, seeking negotiation channels and financial guidance services is an important measure to build sustainable solutions.

In prevention, the analyst highlights financial education as a tool to plan a budget, control expenses, compare interest rates, and understand the total cost of financing. She also warns against promises of easy money, credit without analysis, and online gambling.

This article was prepared based on information from Law No. 11,530, the survey by the National Confederation of Commerce of Goods, Services, and Tourism, and statements by André Cutrim Carvalho and Ana Paula Matos Leal, with data, numbers, and statements preserved as per the consulted material.

Be the first to react!