Portuguese

Portuguese  Spanish

Spanish

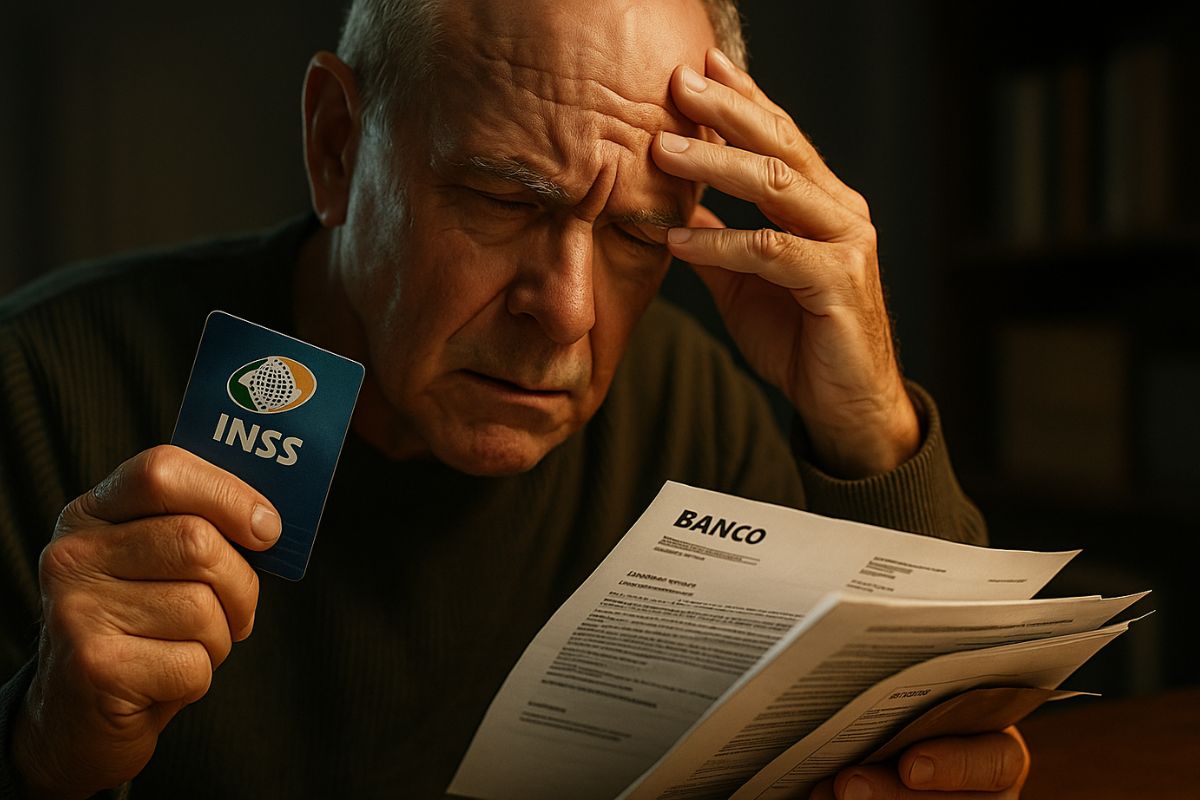

A Judicial Decision Reinforces Consumer Rights In Consigned Loan Cases, Determining The Suspension Of Deductions, Refund Of Values And Compensation For Moral Damages.

The judicial decision that benefits a retiree victim of undue deductions from their social security benefit reignites the debate over the fragility of consigned loan contracts in Brazil. The analyzed case shows that banks and the INSS itself may be held liable for failures in data verification and in the authorization of deductions, with relevant financial consequences.

According to lawyer Carlos Mendes, consumer law specialist, the ruling is an example of how the Judiciary has been applying stricter rules after the change in understanding of the Superior Court of Justice (STJ) in 2021, expanding the protection of retirees and pensioners.

What The Justice Determined

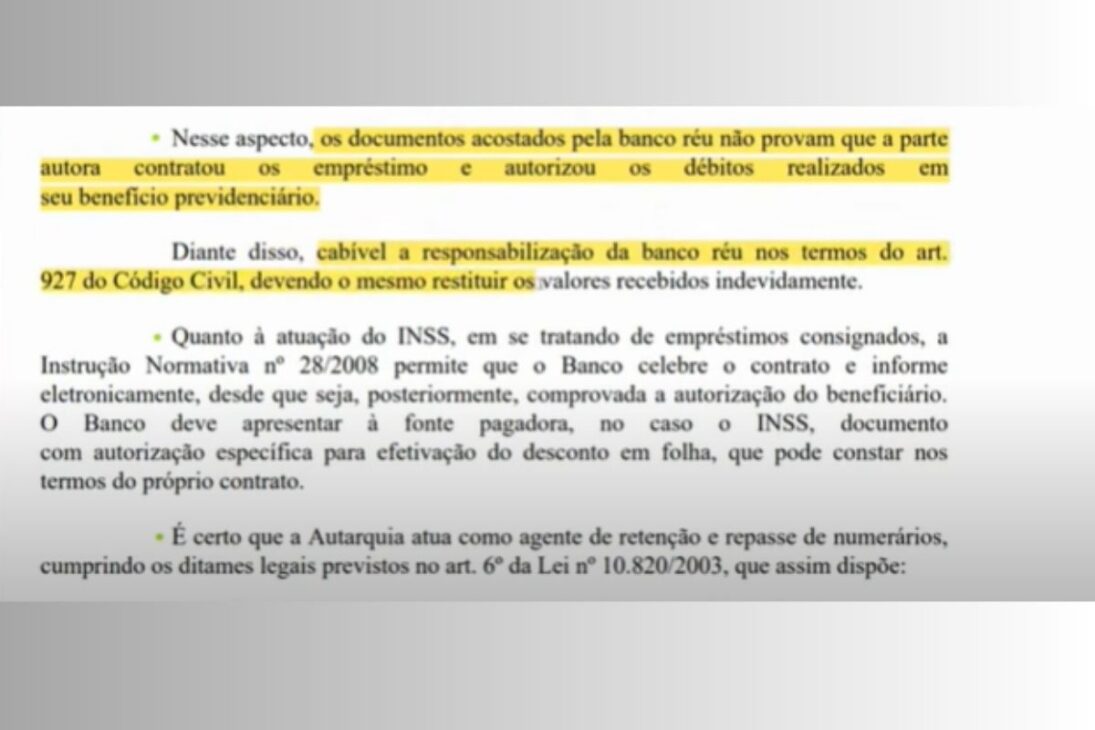

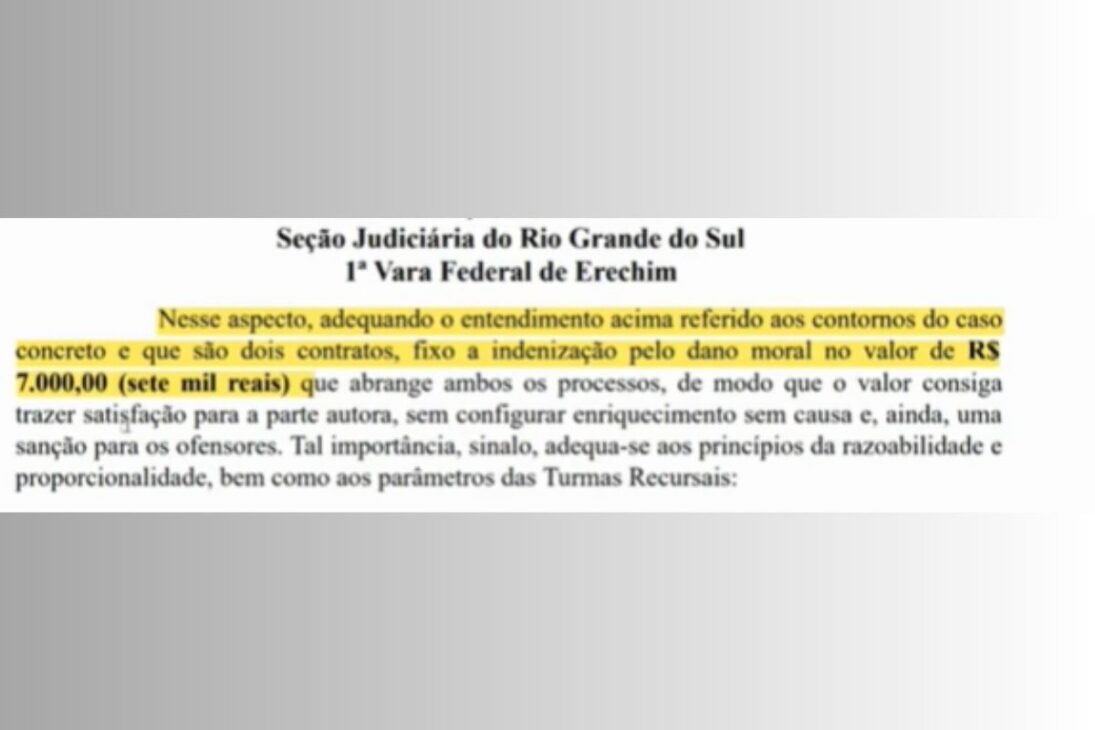

In the process, the defendant bank failed to prove the existence of a valid contract signed by the retiree. Consequently, the judge ordered the immediate suspension of deductions, the refund of charged amounts, and payment of R$ 7,000 in moral damages.

-

Half of Brazilians Prefer Lower Taxes with Private Health and Education, While 44% Opt for Higher Taxes for State-Provided Services, Datafolha Survey Reveals

-

Brazil’s Most Expensive Toll Rises to R$ 40.60 on Route from São Paulo to the Coast, Nearly Matching Bus Fare to Santos

-

As Brazil Expands Social Welfare, Survey Reveals 40% Blame Poverty on Laziness, While 58% Cite Lack of Opportunities

-

China Tightens Control on Antimony, Driving Prices from $22,000 to Nearly $40,000 per Ton as U.S. Rushes to Bolster Strategic Reserves

The decision was based on Article 927 of the Civil Code and Article 42 of the Consumer Defense Code.

In addition to the bank, the INSS was also cited, as it should have verified the accuracy of the data before issuing deductions in the system.

However, its liability was considered subsidiary, meaning it only responds if the financial institution cannot bear the judgment.

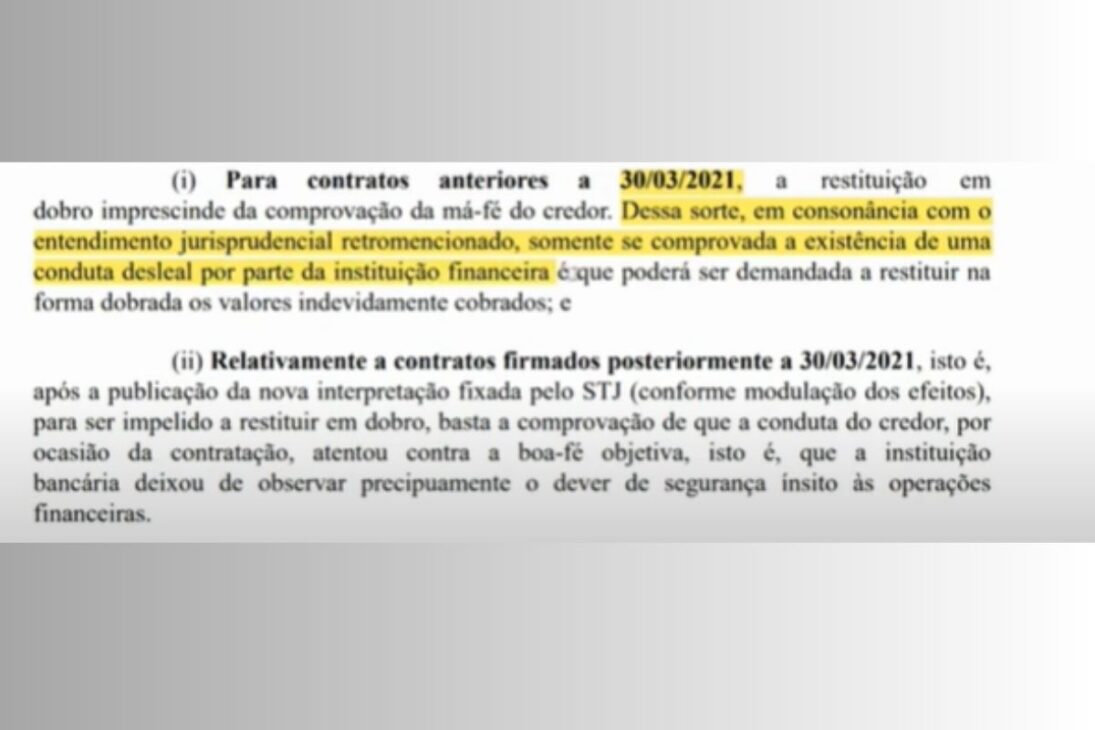

Refund Twice Or Simple: What Changed In 2021

A decisive point of the case involves the rule for refunding amounts. Until March 2021, the refund in double was only possible when there was proof of bad faith by the financial institution.

However, since the new interpretation of the STJ, it is enough to demonstrate failure against objective good faith such as allowing frauds or not adequately verifying the identity of the contractor.

In practice:

Contracts Prior To 03/30/2021 → simple refund, unless proof of bad faith.

Contracts After 03/30/2021 → double refund, even without proof of bad faith, if there is a flaw in the contract.

In the specific case, since the contract was from 2019, the refund was simple.

Nonetheless, the Justice recognized the moral damages, considering that illegal deductions from social security benefits directly compromise the dignity of the retiree.

Why The Problem Is So Common

Brazil has more than 45 million active consigned loan contracts, according to data from the banking sector.

The high demand, combined with a lack of rigor in document analysis, opens gaps for fraud and hiring without due consent.

Many banks allow operations without adequate witness requirements or in-person verification. The result is a growing number of lawsuits.

The Judiciary understands that such practices violate objective good faith and put retirees and pensioners in a vulnerable situation.

Impact For Retirees And Pensioners, Watch The Video From Lawyer Carlos Mendes, Explaining The Case In Detail:

According to lawyer Carlos Mendes, the analyzed case reinforces that harmed consumers can not only recover amounts paid but also receive compensation.

The decision also shows that the INSS can be held accountable when it fails in oversight, even if in a subsidiary manner.

This precedent strengthens retirees and pensioners facing undue deductions, indicating that resorting to Justice can be a viable way to suspend charges, recover losses, and ensure compensation for moral damages.

The judicial decision regarding consigned loans in 2025 represents an advance in consumer protection, but also exposes serious failures in the banking system and in INSS control.

For lawyer Carlos Mendes, the message is clear: contracts need to be more secure, under penalty of institutional accountability.

And you? Do you believe that banks and the INSS are truly prepared to protect retirees against fraud in consigned loans?

Leave your opinion in the comments; we want to hear from those who live this reality in practice.

Tenho empréstimo em meu nome que nunca fiz, c6 bank, falei com um advogado ele disse que não adiantava fazer nada,pois o dinheiro entrou na minha conta poupança e eu não sabia, só descobri que era um empréstimo em outro banco, é muita **** nesse Brasil.

RMC DO BANCO PAN, FAZEM O QUE BEM QUEREM SEM SEREM PUNIDOS PELO INSS E BANCO CENTRAL, CONTINUAM A AGIR INSERINDO JUROS ABUSIVOS E TRANSFORMANDO O CARTÃO CONSIGNADO EM DIVIDA QUE NUNCA TERMINA, MESMO COM O CARTÃO BLOQUEADO. VERGONHOSO !

Fizeram comigo também, e parece que os advogados tem medo de entrar contra essas instituições

Poderíamos nos ajuntamos e procurar um advogado de verdade q façam alguma coisa , estou sendo roubada descaradamente no Bradesco,……

Infelizmente não isso está acontecendo comigo e eu não consigo resolver está sendo descontado do meu benefício BPC dois empréstimos consignado o INSS tira o corpo fora , jogando a responsabilidade no banco e o banco não aceita as provas que eu tenho.

Fizeram no meu consignado, já tá fiz várias reclamações, e eles fingem que nem é com eles

Tem que ir fazer BO……