Portuguese

Portuguese  Spanish

Spanish

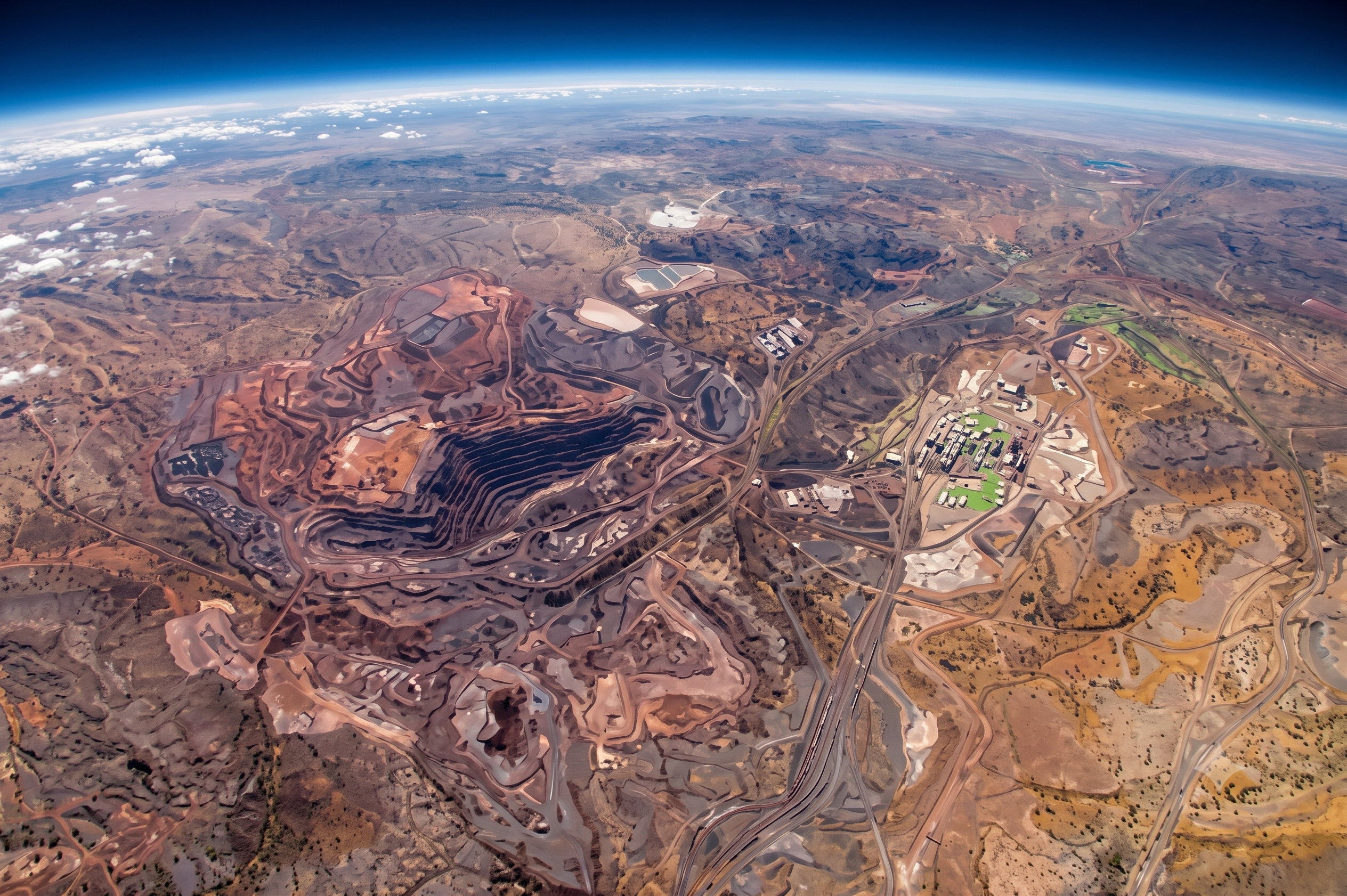

Only 27% of Brazilian territory has been geologically mapped with sufficient precision for mining investment decisions, according to an EY study. The other three-quarters may harbor reserves of rare earths, lithium, copper, and other critical minerals that the world disputes, but which Brazil simply doesn’t know it possesses. Mining accounts for 55% of the trade balance surplus, and the sector has US$ 76 billion in planned investments until 2030.

Brazil sits on a possible geological treasure it cannot see. According to a study by EY, one of the world’s largest consulting firms, only 27% of the national territory has been mapped with a level of precision that allows for decision-making on mining investments. The remaining three-quarters represent an unknown: they may contain significant reserves of rare earths, lithium, copper, and other critical minerals that the global technology, clean energy, and defense industries are increasingly vying for. The problem is that no one has investigated enough to know.

The gap in geological mapping is not just an academic curiosity. Countries that compete with Brazil in the mining market, such as Canada and Australia, have much more complete geological coverage, which allows them to attract investments with lower risk and greater predictability. Meanwhile, Brazil exports raw mineral commodities, processes less than it could, and misses opportunities to add value to a production chain that already accounts for 55% of the trade balance surplus and generates almost R$ 300 billion in annual revenues.

What it means to have 73% of the territory without adequate geological mapping

According to information released by the TIMES BRASIL – EXCLUSIVE CNBC LICENSEE Channel, the 27% geological coverage with precision for investment decisions does not mean that the rest of Brazil is unknown territory. There are preliminary surveys, academic studies, and scattered data over a large part of the territory, but the level at which the subsoil has been mapped does not reach the necessary resolution for a mining company to decide to open a project.

-

Major Appliance Manufacturer Closes Factory in Argentina, Shifts Production to Brazil, and Restructures in Latin America with Mexico Closure, Investing Up to $165 Million

-

China to Revive $3.6 Billion Mega-Dam Project in Myanmar, Stalled Since 2011, Promising 6 GW Capacity and Completion in Eight Years

-

Foreign Company Wins Auction for Brazil’s First Immersed Tunnel, a $1.3 Billion Project with $14 Million Contract Under Federal Investigation

-

China’s Century Megaproject Wows the World: Massive Water Transfer Network Moves Water from Wet South to Arid North, with Ambitious Plans in the Tibetan Plateau Involving Giant Tunnels at Altitudes up to 4,000 Meters

In practice, three-quarters of the country may harbor valuable deposits of critical minerals that no one has discovered because no one has looked with the right lens. While Canada and Australia attract international mining companies with detailed and accessible geological data, Brazil offers potential that relies more on faith than evidence. For Afonso Sartori, EY’s energy and natural resources leader, the translation of this uncertainty is direct: “We have three-quarters of the country where there might be a great treasure, and we haven’t discovered it yet.”

Why Brazil needs to discover its reserves of rare earths and critical minerals

Rare earths are essential inputs for technologies ranging from wind turbines and electric car motors to military equipment and smartphones. China dominates more than 60% of global production and controls almost the entire refining chain, which transforms any new source of supply outside Chinese territory into a strategic asset disputed by Western powers seeking to reduce this dependence.

Brazil already has known deposits of rare earths in states such as Goiás, Piauí, and Bahia, but the lack of comprehensive mapping prevents the country from gauging the true size of its reserves. Minerals such as lithium, copper, niobium, and graphite are also part of the list of critical resources that the world demands and that may be hidden in the three-quarters of the territory that have never been investigated in sufficient depth. Without data, there is no way to plan, and without planning, there is no way to compete.

The obstacles hindering Brazilian mining beyond mapping

The EY study identified four main obstacles limiting the development of the mining sector in Brazil: geological uncertainties, tax insecurity, slowness in environmental licensing, and an incipient capital market. Tax insecurity and slow licensing are known problems for any Brazilian productive sector, but geological uncertainties and the lack of adequate financial instruments are particularities that weigh especially heavily on mining.

A revealing fact illustrates the lack of financing mechanisms: Brazil has ten times more mining companies listed on the Toronto stock exchange than on B3, the Brazilian stock exchange. This means that mining companies operating in the national territory prefer to raise funds in Canada because they find investors there who understand the sector and financial instruments adapted to the stages of exploration and development of mineral projects. BNDES launched a R$ 1 billion fund in 2025 to serve small and medium-sized mining companies, but the amount is modest compared to the scale of the challenge.

The advantages Brazil already has that few countries can match

Despite the obstacles, Brazil possesses trump cards that position it above most global competitors in mining. The industry is strong and mature, with companies that rank among the largest in the world, relatively stable regulations, and, most importantly, the reserves are here. The country is outside conflict zones, which eliminates geopolitical risks affecting competitors like Congo and Ukraine, and its minerals fill global gaps that the energy transition expands each year.

The potential for industrialization is another point highlighted by the study. Brazil exports iron ore, gold, and copper mostly in raw form, adding less value than Canada, Australia, the United States, and China do with their own resources. Each processing stage added within the country generates more revenue and higher margins, transforming a low-unit-value commodity into a competitive industrial product. The challenge is to create the conditions for this value addition to happen here, not abroad.

The US$ 76 billion in planned investments and what is missing to execute them

The mining sector in Brazil has US$ 76 billion in investments planned until 2030, the highest value in the historical series that began to be accounted for in 2014. Almost US$ 20 billion are concentrated in Minas Gerais, reflecting the concentration in iron ore and gold, but the study points to diversification potential for lithium, rare earths, and copper that could expand the participation of other states such as Pará, Bahia, and Goiás.

The problem is transforming plans into execution. For the US$ 76 billion to materialize, Brazil needs more agile environmental licensing, regulatory stability to attract foreign capital, and technical competence in engineering and sustainability, according to Sartori. The geological mapping of the territory is the foundation of everything: without having mapped what exists beneath the earth, the country cannot attract the investments it needs to compete with jurisdictions that have already done this homework.

Do you think Brazil should invest more in geological mapping to discover its rare earth reserves, or would the money be better applied in another area? Tell us in the comments what you think about the country’s unexplored mineral potential and if you believe we can compete with Canada and Australia in this market.