Portuguese

Portuguese  Spanish

Spanish

Even With Traditional Indicators Suggesting Over Supply, Refinery Closures and Backwardated Price Structures Reveal Real Scarcity in the Oil and Gas Sector

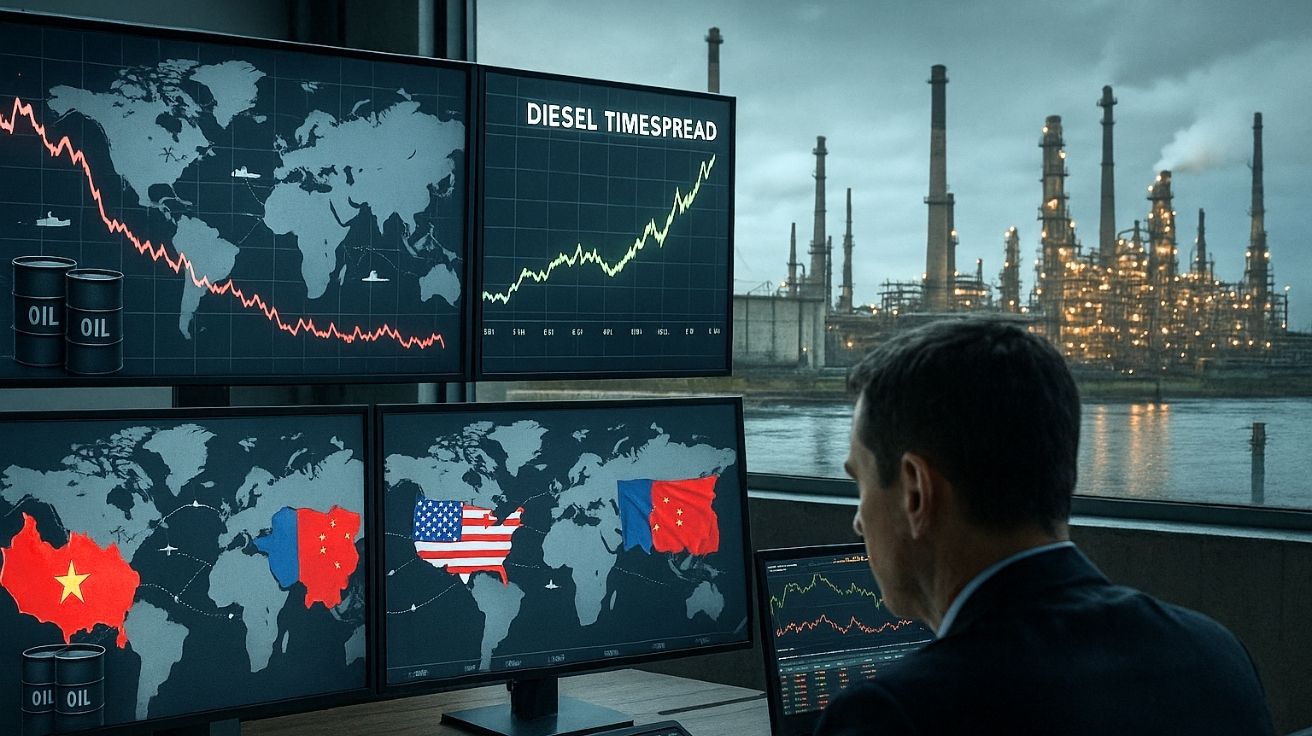

The oil market has entered a period of high complexity and global volatility, with contradictory signals challenging traditional analytical models. Despite a slight decline in barrel prices in recent months, physical indicators such as diesel spreads and refining margins suggest that there is a structural scarcity deepening behind the scenes. Geopolitical instability, refinery closures, and logistical bottlenecks exacerbated by extreme weather events further complicate the scenario of the oil and gas industry. The following information is based on data from the portal oilprice.com

At the beginning of this year, extremely high diesel spreads indicated a tight physical market, even in the face of falling future oil prices. The phenomenon, known as “backwardation,” where short-term contracts are more expensive than long-term ones, is one of the most reliable signs of tightening supply. At the same time, severe weather events in Europe and North America have distorted demand for fossil fuels, making indicators even less predictable.

This scenario is worsened by a scarcity of storage capacity and planned refinery closures in strategic regions. In Europe, over 400,000 barrels per day of capacity will be taken offline this year, while in the United States, the closure of operations such as LyondellBasell in Houston is already impacting supply.

-

Oil Prices Rise as U.S.-Iran Tensions Heighten Concerns Over Global Supply and Energy Market Stability

-

Explosion at QatarEnergy Plant in Ras Laffan Kills 13 and Injures 66; Investigation Rules Out Sabotage

-

Brazil’s Búzios Oil Field Sets Record with 1.2 Million Barrels Per Day, Strengthening Global Leadership in Deepwater Production

-

Petrobras and Equinor Reach Agreement for 50% Stake in Itaimbezinho Block in Brazil’s Pre-Salt Campos Basin

Refineries Cease Operations and Pressure Global Supply of Fossil Fuels

With the closure of major refineries, the oil market becomes increasingly dependent on alternative sources, such as the new Dangote complex in Nigeria. However, this marginal gain in capacity does not compensate for losses in developed countries. This creates regional imbalances and pressures stocks, especially of derivatives like diesel and gasoline.

The movement of barrels from the Middle East and India towards Europe is an important indicator of how the market adapts. When this flow intensifies, it’s a clear sign that Europe is facing internal supply difficulties and needs to seek external alternatives, elevating logistical costs and regional premiums.

The energy sector also faces logistical uncertainties with the persistence of tensions in the Red Sea, affecting tanker traffic through the Suez Canal. Such obstacles increase the transit time of fuels and contribute to higher regional premiums, especially in Western Europe.

Even With an Unstable Economy, Refining Margins Remain High and Sustain Optimism in the Energy Sector

Despite fears of a global slowdown, refining margins remain healthy. Even after a decline in the so-called “diesel cracks”, the sector shows no signs of reduced activity. On the contrary, products such as high-sulfur fuel oil and naphtha continue to perform strongly, sustaining activity in active refineries.

In Asia, China and India are the main players, though with different approaches. China has focused its new refineries on petrochemical products, having little impact on the global supply of liquid fuels. Meanwhile, India is expanding its refining capacity with a focus on both domestic and export markets, although part of the production is tied to rising domestic demand.

These factors help maintain the balance of the oil and gas market, but are not sufficient to fully offset the closures of facilities in the West. The result is a persistent tightening of supply and price volatility in the short term.

Mismatch Between Official Data and Physical Market Signals Raises Alarm Among Analysts and Investors

The phenomenon known as “missing barrel” highlights a disconnection between formal supply and demand data and the conditions observed in the physical market. Even with numbers indicating balance, stocks remain low, especially in intermediate products, revealing a latent scarcity.

This discrepancy is reflected in the spreads between future and spot contracts, and is amplified by policies such as U.S. sanctions on Iran and Venezuela. Any intensification of these restrictions could trigger a “black swan” effect in the market, rapidly driving prices up.

According to an analysis from the portal Oilprice, the oil market today requires a multifactor reading that goes beyond traditional data. An isolated reading of prices or stocks could lead to incorrect conclusions about the balance between supply and demand.

The information was published by the specialized site Oilprice.com, in an article authored by Neil Crosby and reviewed by his editorial team.