Portuguese

Portuguese  English

English  Spanish

Spanish

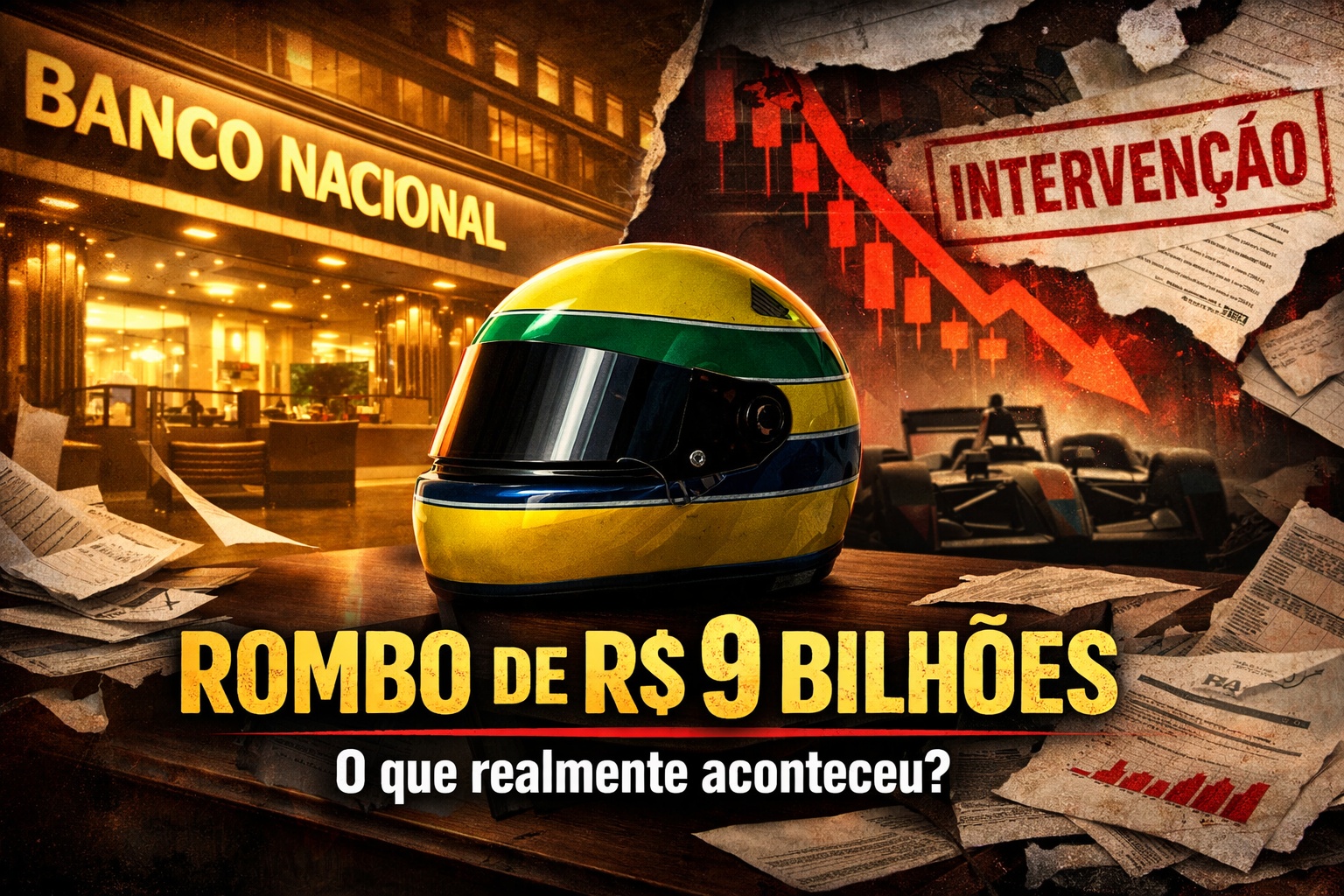

Deficit Exceeding R$ 9 Billion, Accounting Fraud, and Central Bank Intervention Marked the Fall of Banco Nacional in the 90s.

On November 18, 1995, the Central Bank of Brazil declared the Temporary Special Administration Regime (RAET) at Banco Nacional S.A., then the seventh largest private financial institution in the country. The measure, officially announced by the monetary authority and later detailed in public reports and judicial processes, revealed a billion-dollar deficit that exceeded R$ 5 billion at the time, an amount that, adjusted for inflation indices from the period, surpasses R$ 9 billion in corrected values. The collapse exposed one of the largest accounting scandals in the history of the Brazilian financial system.

During the 1980s and early 1990s, Banco Nacional was a symbol of prestige, associated with the successful image of three-time Formula 1 world champion Ayrton Senna. The logo emblazoned on the driver’s helmet solidified the brand as synonymous with modernity and solidity. However, behind the carefully constructed public image, operated a parallel accounting system that masked growing losses and artificially sustained the appearance of solvency.

Political Origins and Aggressive Expansion of Banco Nacional

Founded in 1943 in Belo Horizonte by José de Magalhães Pinto and his brother Valdomiro de Magalhães Pinto, Banco Nacional de Minas Gerais started with an initial capital of 5 million cruzeiros, a significant amount for the time.

-

Six 400,000-year-old teeth found in China contained a protein that was believed to exist only in the mysterious Denisovans: the discovery reveals that Homo erectus interbred with this extinct relative and left a genetic trace that still lives in human populations today.

-

American donated US$ 5,000 to a Chinese farmer to plant trees in the desert, and decades later the money turned into a forest with more than 50,000 trees.

-

Almost no ship sails directly between South America and Australia, and the reason is a combination of the vast distance, winds that circle the planet nonstop, and the absence of ports along the way, leaving the South Pacific as a water desert.

-

More than 85 million homes in China heat water for free with vacuum glass tubes invented at a Chinese university, a cheap technology with no moving parts that faces certification rules and codes in the United States, making installation too expensive.

The political trajectory of José de Magalhães, who held positions such as governor of Minas Gerais and Minister of Foreign Affairs, contributed to expanding the institution’s network of institutional relationships.

In the following decades, the bank adopted an aggressive growth strategy based on acquisitions. It incorporated Banco Sotomaior in 1958, Banco Israelita de São Paulo in 1960, and in 1970, acquired Banco da Grande São Paulo, operating nationally under the name Banco Nacional S.A. In 1972, it also incorporated Banco do Comércio e Indústria de Minas Gerais.

By the 1970s, the bank had a net worth equivalent to approximately R$ 1.2 billion in historical values reported at the time, with annual profits exceeding R$ 200 million. In the 1980s, its annual revenue exceeded R$ 5 billion, consolidating it among the giants of the Brazilian financial sector.

This expansion occurred in an economic environment marked by hyperinflation, widespread indexation, and high monetary volatility. High inflation, which exceeded three-digit annual percentages, distorted balance sheets and allowed financial institutions to mask losses through continuous monetary adjustments of assets.

The Mechanism of Accounting Fraud and the 652 Parallel Accounts

From the late 1980s onwards, the bank began to face significant deterioration in its loan portfolio. Instead of recognizing losses due to delinquency, management created a parallel accounting system internally identified as “Nature 1917.”

There were 652 credit accounts identified that did not appear in the official accounting presented to the market. These accounts were used to record problematic operations as if they were healthy assets.

In technical terms, delinquent loans were artificially maintained as performing credits, with fictitious application of interest and charges.

The accounting effect was the artificial inflation of the bank’s asset. By capitalizing nonexistent interest on unrecoverable operations, the balance sheet presented profits that, in reality, did not exist.

This mechanism allowed the institution to continue distributing dividends between 1990 and 1995, even while technically insolvent since 1990, when its real net worth became negative.

The concealed amount exceeded R$ 5 billion in values of that time, corresponding to about five times the bank’s real net worth. Later estimates indicated that the fictitious operations reached approximately 75% of the internally recorded loan portfolio.

The fraud involved deliberate manipulation of financial statements, noncompliance with accounting standards, and omission of information to the Central Bank. External audits also did not immediately detect the scheme, raising questions about the effectiveness of oversight during that period.

The Impact of the Real Plan and the End of the Inflationary Illusion

The final blow for Banco Nacional came with the implementation of the Real Plan in July 1994. The monetary stabilization drastically reduced inflation and eliminated the so-called “inflationary gain” that many institutions used to compensate for operational losses.

During hyperinflation, the daily monetary adjustment of assets allowed debts to be quickly eroded. With the stabilization of the currency, this dynamic disappeared. Delinquency became more visible and creative accounting lost its support.

Without high inflation to dilute losses and without the capacity to issue new loans to sustain the debt rollover cycle, the deficit became impossible to hide. The institution’s liquidity deteriorated rapidly, forcing the controllers to seek government assistance.

Banco Nacional resorted to the Program for Stimulating the Restructuring and Strengthening of the National Financial System (PROER), created to prevent systemic crises after monetary stabilization. The program allowed interventions with public financing to preserve the stability of the financial system.

Intervention, Division Between Good Bank and Bad Bank, and Liquidation

In November 1995, the Central Bank declared the RAET and removed the institution’s board. An intervenor Board of Directors with broad administrative powers was appointed. The institution then had 335 branches in Brazil, along with three units abroad.

The monetary authority granted more than R$ 5 billion in emergency financing, mostly from the issuance of public debt securities. The strategy adopted followed the model of separation between “good bank” and “bad bank.”

The good bank gathered healthy assets, performing portfolios, and viable operational structure. This part was acquired by Unibanco for about R$ 1.2 billion. The bad bank concentrated the problematic credits and liabilities arising from the fraud, remaining under liquidation supervised by the Central Bank.

The total liability of the institution exceeded R$ 6 billion at the time of intervention. Despite the significant deficit, depositors did not suffer direct losses, as the intervention aimed to preserve deposits and avoid financial panic.

The investigations conducted by the Public Ministry resulted in the indictment of 33 people, including controller Marcos Magalhães Pinto. The charges involved fraudulent management, formation of a gang, and reckless administration. However, the procedural complexity and judicial slowness limited the number of effective convictions.

Regulatory Consequences and Legacy for the Brazilian Financial System

The Banco Nacional case became a regulatory landmark for the Brazilian financial system. The crisis revealed flaws in banking supervision and corporate governance. Following the episode, the Central Bank strengthened oversight mechanisms, demanded greater accounting transparency, and expanded criteria for provisioning for doubtful credits.

The PROER, although controversial for using public resources, was defended as a tool for containing systemic risk. The experience contributed to the consolidation of a more concentrated banking system, albeit more capitalized and regulated.

The stabilization of the Real Plan and the strengthening of oversight significantly reduced the likelihood of fraud of similar scale in the following decades. The episode also underscored the importance of independent auditing, corporate governance, and regulatory transparency.

From a reputational standpoint, the contrast between the public image associated with Ayrton Senna and the internal accounting reality made the scandal even more emblematic. The bank that symbolized speed, victory, and excellence turned out to be supported by a parallel system that masked structural insolvency.

The Collapse That Marked the Brazilian Financial System

The collapse of Banco Nacional was not the result of an isolated event, but an accumulation of misguided managerial decisions, prolonged accounting manipulation, and structural dependence on inflation to sustain artificial results. The monetary stabilization exposed the fragility of a model based on the systematic concealment of losses.

With a deficit exceeding R$ 5 billion in nominal values of the time and an impact surpassing R$ 9 billion in updated values, the fall of Banco Nacional definitively marked the history of the Brazilian financial system.

The episode consolidated the need for rigorous regulation, continuous oversight, and accounting transparency as fundamental pillars of banking stability.

The institution that seemed untouchable at the peak of the 80s and 90s became a classic example of how image, marketing, and aggressive expansion do not replace solid financial fundamentals. The story of Banco Nacional remains a permanent warning about the limits of creative accounting in an environment of increasing regulatory oversight.

-

1 person reacted to this.