Portuguese

Portuguese  Spanish

Spanish

The SAF Tax Reform Suffered Veto From Lula, Keeping The Taxation Of SAFs At 6% And Limiting Benefits To Football.

The SAF tax reform, aimed at the Football Incorporated Companies, underwent a decisive adjustment this Tuesday (13).

When President Luiz Inácio Lula da Silva sanctioned the complementary law project that regulates the new tax system, he imposed vetoes on provisions that would further reduce the sector’s tax burden.

Lula’s veto occurred in Brasília during the final stage of the reform’s regulation.

-

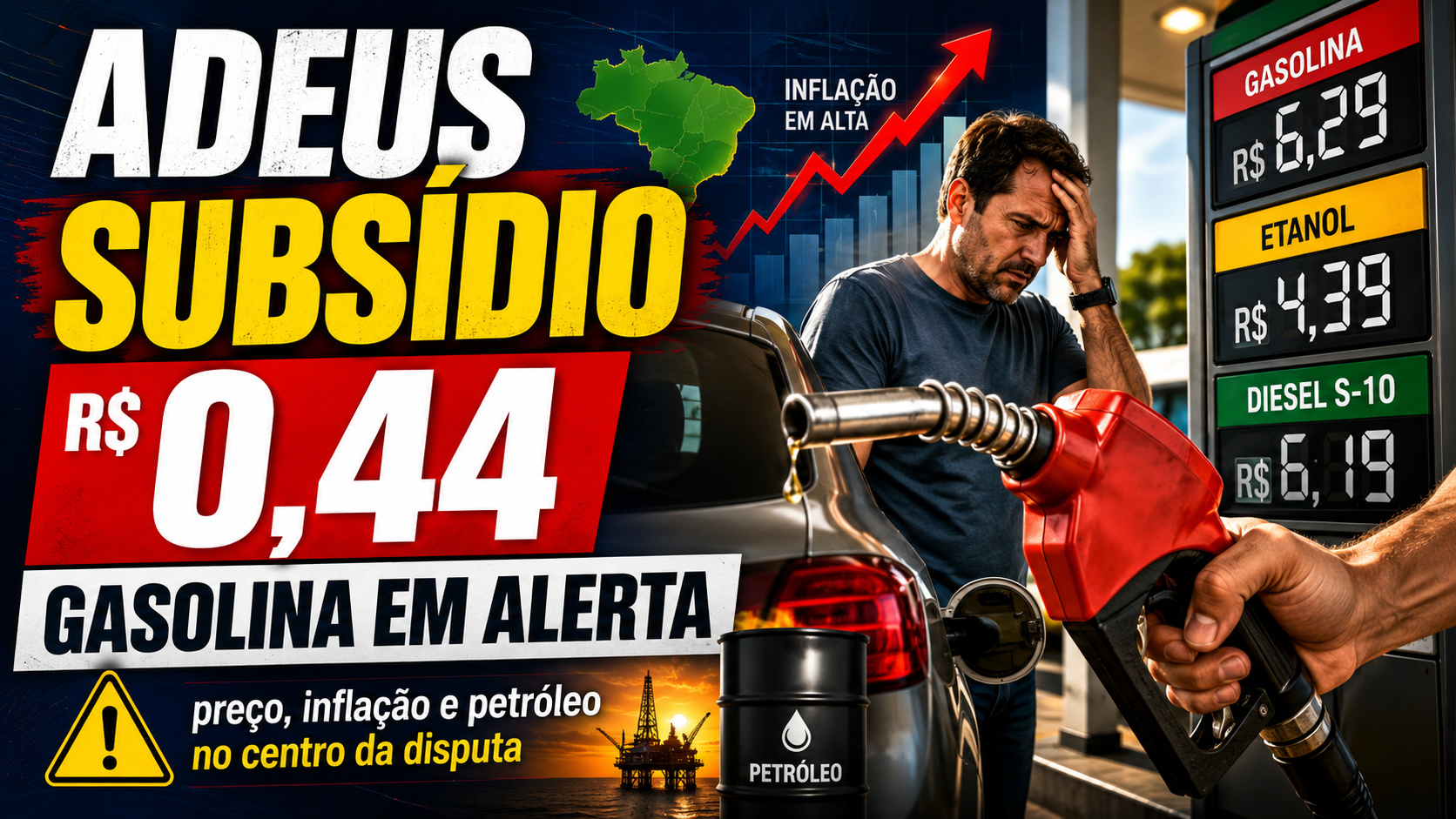

Brazil to Phase Out Gasoline Subsidy, Fuel Prices Set to Rise Amid National Debate

-

Brazil Aims to Boost Critical Mineral Production to 12.2% of Global Output, Targeting Battery and Tech Industries

-

Brazil’s New National Mining Plan Aims to Transform Fertilizer Market and Reduce Foreign Dependency from 87.3% to 34.9%, Boosting Agriculture and Food Production

-

Brazilian Government Plans to Auction Over 500 Road Bridges on São Paulo Stock Exchange in 2026, Promising New Wave of Concessions

It kept the taxation of SAFs at 6%, arguing that new tax benefits would violate the Budgetary Guidelines Law (LDO).

The decision directly affects the tax burden on football by preserving the overall design of the reform and avoiding additional tax waivers.

What Changed With Lula’s Veto On The SAF Tax Reform

The central point of the veto was the exclusion of a provision that reduced the federal rate applicable to Football Incorporated Companies.

In practice, the government considered that this reduction would constitute the creation or reintroduction of a tax benefit, something prohibited by the LDO.

Thus, the Executive maintained the reductions foreseen for the new consumption taxes CBS (Contribution on Goods and Services) and IBS (Tax on Goods and Services), both fixed at 1% each.

As a result, the taxation of SAFs is now composed of 4% of federal taxes that were not altered by the reform, plus 1% of IBS and 1% of CBS.

The result is a total tax burden of 6%, lower than the previous rate, but higher than the level that would have been achieved had the vetoed provision been maintained.

Comparison With The Previous Taxation Model Of Football

Before the tax reform, Football Incorporated Companies were subject to a total rate of 8.5%. Therefore, even with Lula’s veto, there was an effective reduction in the tax burden on football.

However, the government opted for a more conservative model, avoiding a deeper cut that could lead to fiscal and legal questioning.

According to the official justification, the intention was to balance the incentive for the professionalization of clubs with the need to maintain fiscal responsibility.

Thus, the SAF tax reform advances, but without expanding benefits beyond what was already provided in the legal framework.

Additional Vetos Affect Athletes’ Revenues

In addition to the federal rate, the Executive also vetoed provisions that would exclude, for five years, revenues from economic rights of athletes from the tax base of the SAFs’ tax regime.

If maintained, these provisions would further reduce the effective taxation of the companies, increasing the financial incentive for the model.

According to the government’s understanding, these provisions were directly linked to the reduction of rates and, therefore, contradicted the logic of the tax reform and the restrictions imposed by the LDO.

Thus, Lula’s veto reached not only the main structure of the tax but also accessory mechanisms that would impact revenue collection.

Practical Impacts Of The SAF Tax Reform

In practice, the decision preserves a significant reduction relative to the previous model, but signals that the government does not intend to use the reform as a tool to create broad tax exceptions.

For clubs that have already adopted the format of Football Incorporated Companies, the taxation of SAFs remains predictable and aligned with the overall design of the new tax system.

Meanwhile, experts argue that maintaining the burden at 6% still represents a competitive incentive, especially when compared to the previous scenario.

On the other hand, clubs that expected a larger reduction may need to revise short- and medium-term financial projections.

Next Steps After Lula’s Veto

The vetoes applied to the SAF tax reform will be officially detailed next Wednesday (14), with publication in the Federal Official Gazette.

After that, the National Congress will be able to analyze the vetoed provisions and decide whether to uphold or overturn the presidential decision.

Until then, the scenario remains defined by the new rate of 6%, consolidating a new level for the tax burden on football in Brazil.

The measure reinforces the government’s strategy of promoting structural changes in taxation without giving up fiscal control.

Even in sectors with significant economic and social appeal, such as professional football.